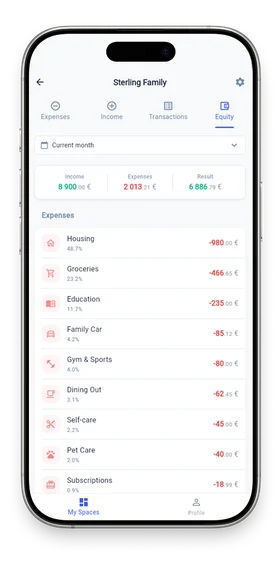

Set a financial target and a date. Our AI calculates your required monthly savings and predicts if you'll reach your goal based on your actual spending velocity.

Everything you need for financial clarity

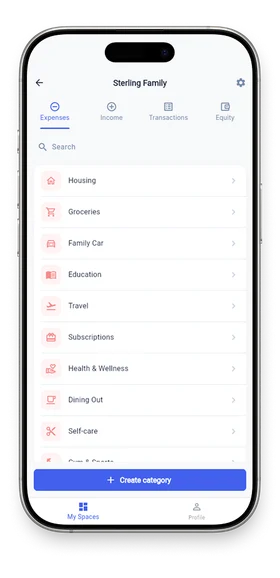

Key features of Small Metrics Money

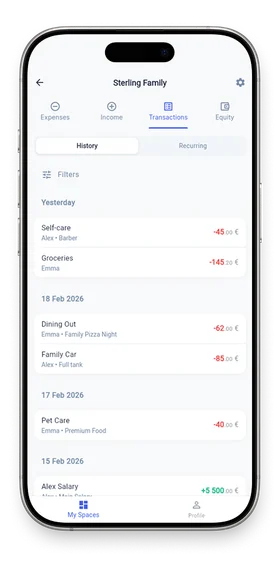

Reconcile your app data with actual cash on hands and bank accounts. Instantly see your true net cash flow and identify lost funds.

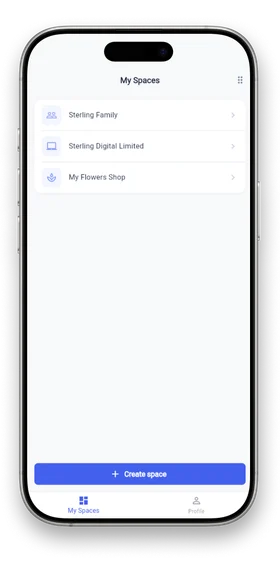

Invite your spouse to your Family space or your accountant to your Business space. Set Admin or Member roles for secure joint budgeting.

Support for 160+ world currencies with automatic exchange rate updates. Spend in USD, earn in EUR, and view analytics in your preferred base currency.

Budget Interface

A quick look inside the app.

Security matters

We know that technical terms can sound dry. But behind these complex words is a simple, human promise: your data belongs exclusively to you. We do not sell your information to advertisers. We simply build a secure vault for your peace of mind. Read the privacy policy.

☁️ Hosted on AWS (EU)

🛡️ GDPR Compliant

🔒 256-bit Encryption

Frequently Asked Questions

Absolutely! That is the core feature. You can create multiple isolated "Spaces". The transactions and analytics in these spaces will never mix.

You can add transactions in 160+ currencies. Our system automatically converts them into your Space's default currency using daily exchange rates.

Yes, you can invite members via email and assign them "Member" or "Admin" roles.

We take security very seriously. All data is encrypted and hosted on secure AWS servers located in the EU.

Ready to take control of your money?

Join users who have already organized their finances.

Open Web App Free to use. No credit card required.

Documentation

Latest updates

-

How to track your financial obligations and loans

-

How to track issued loans and their impact on your net worth

-

How to track real estate, vehicles, and equipment for your equity calculation

-

How to rearrange the display order of your workspaces

-

How to clear inactive budgets from your main screen

Articles

Recently added to the Blog

- Comparing Kubera with Small Metrics

From passive asset monitoring to active capital growth

- Comparing Honeydue with Small Metrics

From simple couple tracking to joint capital

- Comparing Zenmoney with Small Metrics

From utilitarian tables to a premium interface and forecasts

- Comparing Copilot with Small Metrics

AI - automation and premium design without Apple lock - in

- Comparing Lunch Money with Small Metrics

Global tracking for digital nomads without compromises

Comments

Recent user comments

-

actually, tracking every single coffee is a massive bottleneck for your personal bandwidth. with all due respect, if you need an app to micromanage daily expenses, you just have an income problem. modern approach uses credit limits as a free leverage to optimize cash flow, you don't need to track it daily. high-level portfolio alignment is what really matters, but good luck counting pennies i guess

-

The underlying premise of this article—that "utilitarian tables" and granular micro-control are somehow detrimental and should be replaced by "elegant color coding" and AI approximations—is fundamentally flawed.

It is rather amusing to observe users in the comments experiencing a sudden epiphany regarding food delivery fees. While your belated realization concerning the marginal utility of a cold burger is quaint, it perfectly illustrates why hiding your financial reality behind automated push notifications and a minimalist 8-pixel grid is a catastrophic paradigm for personal wealth. If you are not confronting the raw, unadulterated numbers in a comprehensive ledger, you are not managing your money; you are merely spectating your own financial decline.

Financial security is not achieved through "unobtrusive background processes." It requires aggressive, uncompromising micro-management. Every single transaction, down to the exact cent paid for a streaming subscription or the maintenance of a premium vehicle, must be deliberately recorded and mathematically reconciled. This deliberate friction forces a psychological reckoning. When you have a substantial mortgage to service and a specific standard of living to maintain, delegating your budget to a multimodal neural network that spits out a theoretical "Equity Forecast" is an exercise in perilous delusion. You need the granular data to understand the true velocity of your capital and the brutal reality of compound interest.

Furthermore, the ubiquitous obsession with porting every aspect of personal management into a digital SaaS ecosystem—evident from the myriad of "Tasks Comparison" links cluttering the sidebar—is a testament to the modern tech-bro’s refusal to understand cognitive load. Automating your financial data aggregation via API is one thing, but attempting to manage your daily objectives and budget planning through yet another cross-platform Flutter application is inherently inefficient. Motor memory and the tactile resistance of writing your strategic priorities in a Leuchtturm1917 with a well-weighted fountain pen will always yield far more tangible productivity than any digital Kanban board.

It takes an exhausting amount of meticulous, manual tracking to sustain a demanding lifestyle without the underlying mathematics collapsing. I am currently analyzing these application architectures while a rather bleak, relentless blizzard obliterates the visibility outside my window, nursing my third espresso to compensate for a chronic sleep deficit, and frankly, the dichotomy here is stark. You can either manually architect your financial and operational reality through rigid analog discipline and strict tabular tracking, or you can let an algorithm gracefully color-code your path to insolvency. The choice is yours :)

-

Hello everyone. I am new here, sorry if my English is not perfect. I am reading this thread for a few days and finally decided to register.

@User_1 and @User_2, you have a good point about simplicity, but with all due respect to your paper notebooks, this method is mathematically primitive and does not scale. Actually, statistically speaking, manual tracking on paper fails immediately when you have more than three active credit lines or dynamic interest rates.

I work as a QA engineer and my financial situation is... a complex mathematical problem right now. I have a big debt problem after some bad crypto investments, and I strictly track my negative net worth. A physical notebook can not calculate daily interest compounding or predict default dates.

Regarding the article, the Smart Import with Gemini AI sounds good for marketing, but as a technical person, I see a huge bottleneck. LLMs like Gemini have a known hallucination rate. If the neural network parses your bank statement and accidentally categorizes a "credit card refund" as a "regular income", your entire 10-year Equity Forecast will be completely destroyed.

This is why I do not use commercial trackers and built my own system:

- I use my bank's open API to pull raw JSON transactions into Notion.

- I wrote a simple Python script to parse the data using strict Regex. I do not trust AI with this, Regex is 100% predictable.

- To mathematically calculate which micro-loan is eating my salary faster, I use dynamic formulas. Here is a basic piece of code from my dashboard to calculate daily debt cost:

if(prop("Status") == "Active", prop("Debt Balance") * (prop("APR") / 365), 0)

You just can not update this in a paper notebook every single day. And AI parsing is too risky for this level of micro-control. You need absolute precision when you are in the red.

I am thinking about writing a custom Zapier webhook to model my debt restructuring automatically based on EURIBOR changes. Does anyone else use custom API scripts for tracking negative balances, or maybe my setup is too complex and I am overthinking it?

-

I am utilizing this thing immediately to conserve my times... but does it calculate the futures automatically like we manually did back in my youths?

-

Im just searching for how to track business expenses for freelance astrological life coachings but honestly observing your cash directly collapse the quantam wealth waves anyway so you should literally just rely on pure financial vibes instead 🥱💸

-

Well I read this article and I am honestly very inspired to download this app right this second. I usually doubt everything on the internet because companies always hide the real numbers... but this actually makes a lot of sense to me. Back in my day we just balanced a checkbook at the kitchen table and we did not need fancy tools.

But anyway I really need the best personal finance management app for multiple international bank accounts to track my money. I am losing so much cash and I demand proof of where every single penny goes. So I am going to set this up right now and finally take control of my savings.

I do have one very quick question before I start though... Does Small Metrics offer automatic import of statements from around the world?

-

i am literally sitting on the subway rn so bored but reading this made me so hyped for my money goals. small metrics sounds lowkey amazing because me and my partner always argue about bills and stuff but honestly my dog ate my last budget planner anyway lol 🐕. we have been searching for the best family budget app for expats with multiple currencies since we moved to europe but supposably other apps just trap you in dollars.

it is definetly a huge flex that you guys have 166 currencies and that equity forecast thing to see 10 years ahead 💸. i tried doing that on a spreadsheet once but then i remembered i need to buy groceries for dinner tonight. wait i do have a quick question about that gemini ai smart import thing you mentioned 🤔. does it automatically translate the foreign bank receipts into english or do we have to manually type the translated words out.

-

Well back in my day we just used a simple paper notebook for our money... but I really love this new app you made. It is just super cool to see all the new things. The smart import stuff sounds really amazing actually.

I was searching for a good personal finance management app with ai bank statement parsing for freelancers because I travel a lot now... But I have a quick question about the limit control section you wrote.

You mention setting a limit in any currency and the system convert it to the base one. Does it use the live exchange rate for that every day or can I lock in my own rate... I just want to know how that works before I start using it for my overseas trips.

-

I just read this Comparing Zenmoney with Small Metrics article and it seriously blew my mind 🤯 I am setting up my account literally right now because I need to stop wasting cash.

But honestly I just need to vent about food delivery apps real quick 😡 I ordered a basic burger today and the fees was literally more than the food. The driver always get lost so I waste my whole evening just waiting around for cold fries. That is so much lost time and money for zero reason bro.

I could of cooked a meal in ten minutes and kept my twenty bucks 💸 I am going to use this tracker right this second to calculate exactly how much those delivery guys steal from me.

I am relatively new to this specific community, but passing through this thread, I find it quite fascinating that you equate systemic telemetry with a "personal bandwidth bottleneck," @User_1. Purely from a project management and systems architecture standpoint, your argument is built on a rather dangerous logical fallacy.

With all due respect to your "modern approach," claiming that relying on credit limits as "free leverage" negates the need for granular expense tracking is the managerial equivalent of running a massive Agile development cycle while ignoring the daily burn rate. You are assuming the high-level roadmap will somehow magically cover the server costs and technical debt.

Let’s dismantle this operational optimism for a moment:

Attempting to build a sustainable financial architecture solely on macro-asset monitoring without a grounded daily tracker is much like trying to architect a scalable backend while battling a severe fever during a gale-force storm outside. You can try to focus on the majestic big picture all you want, but the immediate, unmanaged symptoms and the structural shaking will eventually bring the entire system down.

If blinding yourself to daily cash flow while floating on credit leverage works for your personal risk tolerance, I genuinely applaud your optimism. But for those of us who prefer to engineer actual control over our operational resources—rather than just hoping our income outpaces our blind spots—a unified system is structurally superior.